Study | Sensitivity Analyses 2022

Key conclusions

The sensitivity analysis confirms the key takeaways from the main analysis, showing that a robust selection of basic scenarios was made. Additional conclusions are presented on the challenges for a fast electrification and on the impact of choices and technology assumptions on costs.

The conclusions from the main analysis for 2030 and for the 2050 demand sectors remain the same.

- By 2030, in all scenarios -including sensitivities- solar PV capacity needs to increase by a factor 4 and wind onshore and offshore by a factor 2. In all sensitivities, there are 1,5 million residential homes and commercial buildings with heat pumps and 2 million electric cars on the Belgian roads.

- By 2050, there is no more fossil fuel used except small quantities in some industries.

- On the supply side, low carbon electricity is the largest resource for the total energy system. There is no uptake of local green hydrogen production before 2030.

The Central and the Clean molecules scenarios have a structural deficit of low carbon resources.

- The interconnection import capacity increases from the current 6.5 GW to 13 GW by 2040 and yet, there is not enough electricity. In fact, there is a structural deficit of low carbon resources, especially in the period 2030-2040. The imports from the neighbouring countries as well as the import capacity are not sufficient, and importing of molecules is costly. Solar electricity is very cost efficient however for some demands, it is too costly to match solar production profile with demand profiles.

- Without enough low carbon electricity, some demand sectors will not be able to electrify and will reinvest in fossil-based technologies. In other words, there is a high risk of stranded assets. A stranded asset is for example a replacement of an existing diesel truck with a new diesel truck that cannot be used any longer even before reaching its end of life.

It is important to have clean electrons timely.

2030 is an important milestone but also the period 2030 to 2040 is crucial. The most cost optimal net-zero emission scenario is a scenario in which Belgium looks for renewable energy resources beyond its borders.

- Demand electrification can happen in time only if zero carbon electricity reaches 70TWh by 2030 and 150 TWh by 2040. Starting from currently 22 TWh, electricity production from renewable resources must triple by 2030 and must increase sevenfold by 2040.

- Access to additional offshore wind is the most important factor to lower the energy system cost because it can enable early electrification of demand sectors. In doing so, around 19 GW of offshore is active by 2040 (8 GW in Belgian waters + around 11 GW additional).

- Based on our assumptions, new small modular nuclear power plants (SMR) and offshore wind have a comparable electricity cost however SMR comes too late for guaranteeing a smooth transition in the demand sectors.

- Much of the energy will be imported from nearby sources and in all scenarios, we will import far less energy than we do today.

KEY TAKEAWAYS

-

Current (2020) renewable electricity generation is

22 TWh -

By 2030 zero carbon electricity reaches

70 TWh

in all scenarios -

By 2040 zero carbon electricity has to reach

150 TWh

to electrify demand timely

It is more important to have clean electrons timely than to have the optimal mix.

- All scenarios that have at least 15 GW offshore wind power by 2040, have very similar total costs.

- Regarding cost efficiency in the period 2030-2040, offshore is followed by onshore wind and solar electricity. In the sensitivity where we enforce a high level of solar in 2040 (‘Electr. PV 75% Push’), photovoltaic power starts to outcompete onshore wind power and the less favorable offshore wind parks.

- Introducing new small modular nuclear power plants (SMR) has a major impact on the electricity mix in 2050, mainly reducing PV and hydrogen needs.

- The investments in small modular nuclear power plants get outcompeted if Belgium manages to get access to 32 GW of additional offshore wind power or if the cost of SMR is above 10800 euro per kW.

- Electrification of demand sectors is largely independent from the electricity mix. The only effect we observe is that high levels of solar power trigger heat storage with basic electric heaters.

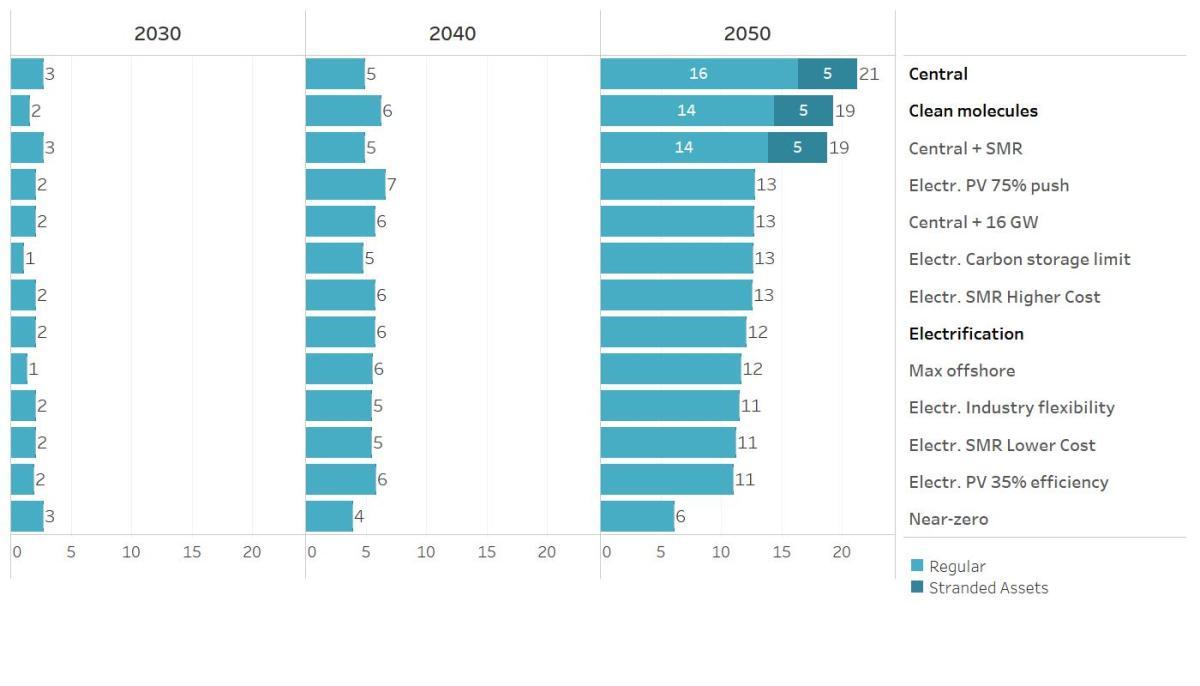

Annual Costs (B€)

Summary for each sensitivity

This section covers the main conclusions for each sensitivity run. We provide insights on offshore wind, photovoltaic efficiency, Small Modular Reactors (SMRs), industry flexibility, carbon storage limitation and the carbon reduction trajectory. All sensitivity runs are based on the Electrification scenario, except the sensitivities on adding only wind offshore or SMRs to the Central scenario and except the Near-zero sensitivity.

Offshore wind

Before 2040, access to additional zones for offshore is key because it is the cheapest option to enable a fast electrification of demand sectors. In all scenarios with additional 8 GW access, wind offshore capacity amounts to 8 GW by 2030, 12 GW by 2035 and between 15 and 19 GW by 2040. Additional offshore wind zones beyond the extra 16 GW have a smaller cost impact (scenario Max offshore).

Industry flexibility

Allowing additional capacity for key electrified industry processes provides an additional form of flexibility by 2050. The additional industrial flexibility decreases the need for controllable load in a more cost-effective way. While the new nuclear capacity in 2050 is lower, the capacity of onshore and offshore wind is slightly higher. Largest difference however is the PV capacity. The PV capacity is 6,4 GW higher than the Electrification scenario and amounts to 45,9 GW in 2050.

Carbon storage limitation

When CO2 storage is limited to 5 million ton per year, net emissions increase by around 10 million ton in 2030. By 2050, there is an increased use of captured CO2 for feedstock production (2 million ton per year) and increased electrification in the chemical sector.

Near-zero emission

With a CO2 price of 350 €/ton, CO2 is reduced by 85% in 2050. The remaining 15% come from sectors where reducing all CO2 is not cost-efficient if only this carbon price is applied, such as heavy-duty transport. This result is very sensitive to the assumption of maintenance cost.

PV efficiency and cost

PV panels are very cost efficient in the next years to come. After reaching 20% of electricity generation, the benefit from PV panels diminishes. With an increased efficiency of 50%, equivalent to a cost reduction of 33%, electricity generation from PV increases with 50%. When enforcing a high level of solar in 2040 (‘Electr. PV 75% Push’), photovoltaic power starts to outcompete onshore wind power and the less favourable offshore wind parks.

Small Modular Reactor (SMR)

The SMR technology is always present if allowed, except if there is a total of 40 GW of offshore wind capacity. Allowing access to SMR in scenarios increases the electricity demand by 5-9% due to the lower electricity price, and lowers electricity imports. A 600 euro per kW investment cost reduction/increase leads to an increase/decrease of the SMR capacity by 1 GWe. The capacity factor of nuclear is above 75% in all scenarios except the sensitivity scenario with a lower investment cost (4500 euro per kWe) where it reaches 64%.